Skip to content

Skip to content

Corporate tax starting in June 2023, Free Zones Businesses and Qualifying Free Zone Persons may be subject to a 0% or 9% corporate tax, depending on their qualifying income. On the other hand, Mainland businesses were subject to a standard 9% tax rate based on their taxable income exceeding AED 375,000. The Federal Tax Authority (FTA) and the Ministry of Finance have announced a new corporate tax policy, and the UAE is prepared to implement it as of June 2023.

9% is the legal corporate tax rate. In this article, on corporate tax, we will discuss the system in the United Arab Emirates and analyze how corporate tax affects firms in both the Mainland and the Free Zone.

Cabinet’s decision on corporate tax for free zone persons?

On May 30, 2023, Cabinet Decision No. 55 of 2023 was released. It was about figuring out qualifying income for a qualifying free zone person under Decree-Law No. 47 of 2022, which is the federal law on taxes for companies and corporations (hereafter called the “CT Law”).

Also, on June 1, 2023, the Ministry of Finance released Ministerial Decision No. 139 of 2023, which discusses what activities are “qualifying” and “excluded” under the CT Law. This decision should be read along with Cabinet Decision No. 55 of 2023 for a complete understanding of the suggested rules.

Both decisions were made official the day after they were made public.

Decision No. 55 of the Cabinet of 2023 on

Figuring Out What Income Is Qualifying for the Qualifying Free Zone Person being in line with Federal Decree-Law No. 47 of 2022 on how to tax businesses and corporations.

After going over the Constitution, Federal Law No. 1 of 1972 on the Powers and Duties of Ministers and the changes made to it, Federal Decree-Law No. 13 of 2016 on the Creation of the Federal Tax Authority and its Changes, Decree No. 28 of 2022 from the government on tax procedures, and Decree-Law No. 47 of 2022 from the federal government on how businesses and corporations are taxed, Based on what the Minister of Finance said and with the Cabinet’s approval, it was decided:

What It Means The rules in Federal Decree-Law No. 47 of 2022 about how to tax corporations and businesses will be used. With exception to that, the following words and phrases will mean what they say, unless the situation says otherwise. requires otherwise:

Key points: Corporate tax in the free zone

Domestic Permanent Establishment: A place of business or other form of presence of a qualifying free zone person outside the free zone in the state.

Qualifying Activities: Any activities approved by the Minister and carried out by a Qualifying Free Zone Person that bring in Qualifying Income

Excluded Activities: Any activities listed in a Ministerial decision that a Qualifying Free Zone Person performs and that result in non-Qualifying Income.

Non-Free Zone Person: Any Person who is not a Free Zone Person

Commercial Property: Immovable property or part thereof:

(a) used exclusively for a Business or Business Activity.

(b) not used as a residence or accommodation, including hotels, motels, bed and breakfast establishments, or serviced apartments.

Corporate Tax Law: Federal Decree-Law No. 47 of 2022 on How Businesses and Corporations Are Taxed”.

Limits of the Application: The rules in this Decision shall apply to Qualifying Free Zone Persons.

Qualifying Income:

1 To make Article work (18) of the Corporate Tax Law, the Income of the Qualifying Free Zone Person shall include the below categories of Income, provided that such Income is not attributable to a Domestic Permanent Establishment or a Foreign Permanent Establishment by Article (5) of this Decision or to the ownership or exploitation of immovable property by Article (6) of this Decision:

a. Income derived from transactions with other Free Zone Persons, except for Income derived from Excluded Activities.

b. Income derived from transactions with a Non-Free Zone Person, but only regarding Qualifying Activities that are not Excluded Activities.

c. Any other income provided that the Qualifying Free Zone Person satisfies the de minimis requirements under Article (4) of this Decision.

2. For paragraph (a) of Clause (1) of this Article, Income will be considered derived from transactions with a Free Zone Person where that Free Zone Person is the Beneficial Recipient of the relevant services or Goods.

3. For the purposes of this Article, the word “Beneficial Recipient” shall mean a person who has the right to use and enjoy the service or the Good and does not have a law or contractual duty to pass on such service or good to another person, and the term “good” shall mean tangible or intangible property that has economic value in dealing, including moveable and immovable property.

4. Qualifying income shall include income derived from any person where such income is incidental to the income under paragraphs (a) or (b) of Clause 1 of this Article.

5. To determine whether a Qualifying Free Zone Person has a Domestic Permanent Establishment, the provisions of Article 14 of the Corporate Tax Law shall apply, and the expression “Qualifying Free Zone Person” shall be used instead of the expression “Non-Resident Person”, and the expression “geographical areas outside the Free Zones in the State” shall be used instead of the word “state,”, wherever used in that Article.

De minimis Requirements

1. The de minimis requirements shall be considered satisfied where the non-qualifying revenue derived by the qualifying free zone person in a tax period does not exceed a percentage of the total revenue of the qualifying free zone person in that tax period as specified by the minister or an amount specified by the minister, whichever is lower.

2. Subject to Clause (3) of this Article, the following provisions shall apply: a. Non-qualifying revenue is revenue derived in a tax period from any of the following:

1) Excluded Activities,

2) Non-qualifying activities, where the other party to the transaction is a non-free zone person.

b. Total Revenue is all Earned by a qualifying free zone person in a tax period.

3. The following Revenue shall not be included in the calculation of non-qualifying Revenue and Total Revenue:

a. Revenue attributable to immovable property located in a free zone derived from the following transactions:

(1) Transactions with non-free zone persons in respect of commercial property

(2) Transactions with any person regarding immovable property that is not commercial

b. Income from a permanent establishment in the United States or a foreign country that belongs to a qualified free zone person.

4. For this Article’s purposes, a qualifying free zone person and its permanent or foreign establishment in the United States or a foreign country will be treated as if the establishment were a different person from the qualifying free zone person.

In conclusion

Free zones in the UAE have had many tax breaks for a long time. Some of these are 100% foreign ownership, 100% customs and VAT exemptions, 100% returns on capital and earnings, and company tax exemptions. Businesses in the UAE’s free zones will have to register, file a corporate tax return, and send in tax reports every year after the new corporation tax goes into effect. They will also have to follow all other legal requirements. Therefore, it is clear that free zones are subject to corporate tax. The tax rate can range from 0% to 9%, based on the type of income.

The UAE’s economy will soon be taxed in a new way. Businesses in free zones should be aware of the biggest problems they must solve. Free Zone businesses could use the help of corporate tax experts like Highmark in Dubai to understand complicated tax rules and make sure they follow the rules. Our skilled team can look at the Corporate Tax rules that apply to your business and help you find the best corporate tax solutions. We can also offer full regulatory, compliance, and tax consulting support to improve your company’s standing in the UAE’s business community.

Contact the pros at Highmark Tax Consultants right away for reliable tax advice and questions about UAE corporate tax on free zones.

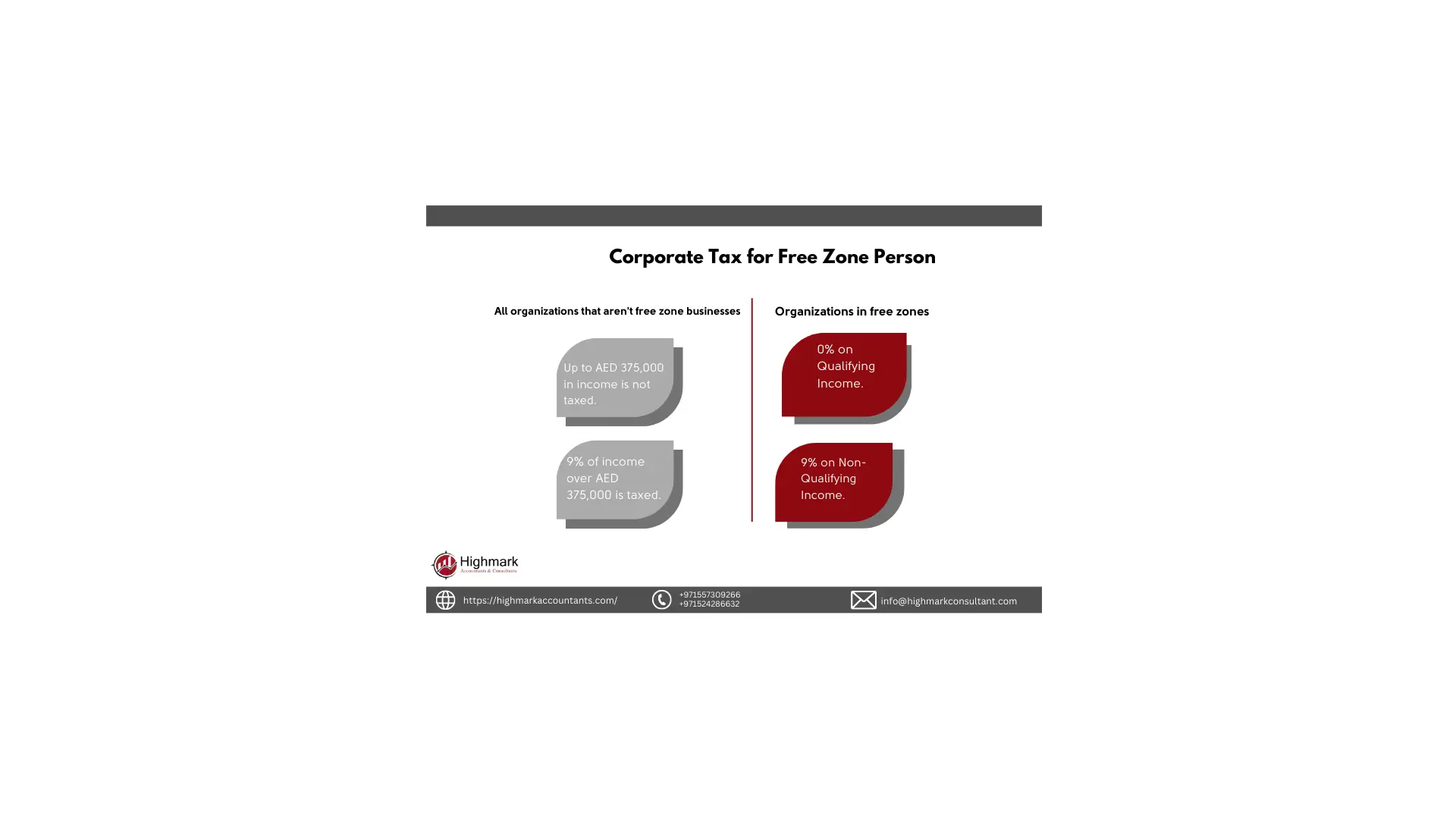

Graph content

All organizations that aren’t free zone businesses

A) Up to AED 375,000 in income is not taxed.

B) 9% of income over AED 375,000 is taxed.

Organizations in free zones.

0% on Qualifying Income.

9% on Non-Qualifying Income.

corporate tax-free zone

corporate tax on free zone

corporate tax uae

UAE tax

corporate tax rate

corporation tax in Dubai

corporation and taxes

corporate taxation

corporate tax UAE free zone

corporate tax UAE 2023

corporate tax uae

corporate tax services in uae

corporate tax on free zone

corporate tax law uae

corporate tax law

corporate tax law in uae

corporate tax in dubai free zone

corporate tax for free zone companies

corporate tax consultant in dubai

corporate tax accountants

corporate income taxation

corporate income tax uae

Corporate Income Tax Dubai

company taxes in dubai

business tax in uae